A majority of OEM’s integrates radar technology for new ADAS applications. Radar is often combined with other sensors as it provides valuable information to ensure better safety and helps in collision avoidance. OEM’s demand is well supported by Tier1’s offer with strong product portfolio. Analysts identified almost 50 active product references existing on the market. Market is very dynamic with strong competition and continuous product developments.

With the recent strong focus on safety, the market potential for ADAS has been extended to mid-end cars resulting in a production volume increase. Coupled to the fact that radars are well considered and employed by many brands: in 71% of cases for AEB.

The automotive radar market consequently benefits from a 23% CAGR between 2016 and 2022. AEB application is the main driver for the 77 GHz radar market growth. Yole Développement announces a global radar market reaching US$7.5 billion in 2022, at the module level. “This growth should be accelerated with the autonomous car market,” comments Cédric Malaquin, Technology & Market Analyst, RF Devices & Technologies at Yole.

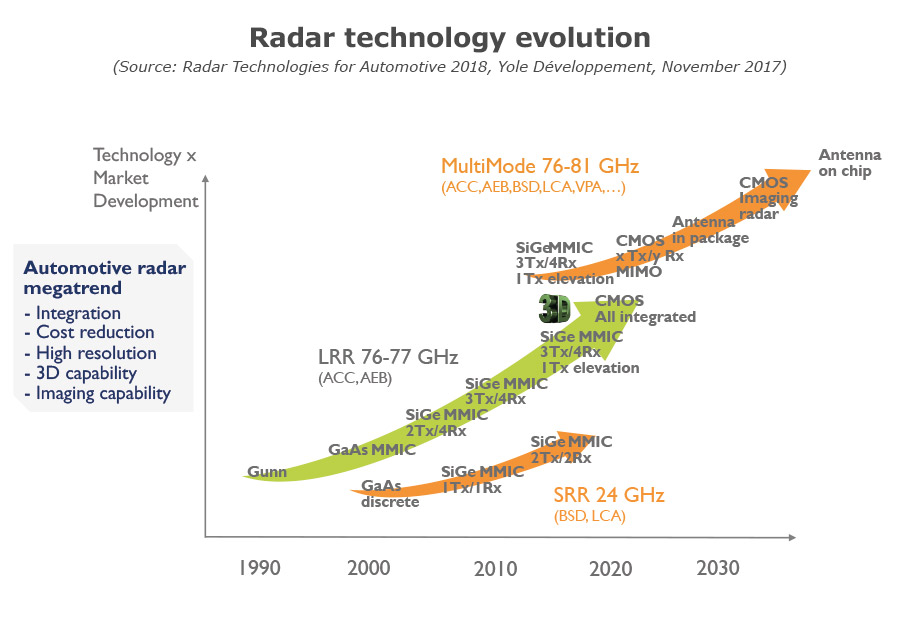

Another trend with the advent of autonomous driving is the use of corner radar for the car 360° surveillance. These short and mid-range radar are supported by 24 GHz and more recently by 79 GHz module. The latest one being more suited for high resolution tracking which will be desirable for tasks such as target separation or even object recognition. Corner radars will be a must have for redundancy with other sensors such as camera or even Lidar for high-end robotic cars.

In parallel, semiconductor’s manufacturers deliver high performance solutions that enable mm-Wave Radar to be operated in a reliable and accurate manner which is critical for safety functions. They propose a wide technology offer with GaAs, SiGe BiCMOS and RFCMOS platforms.

Innovative startups such as Metawave and Uhnder, bring disruptive technologies to the market to support high resolution sensor requirements either with ultra-thin steerable beam and AI engine for a deep learning approach or with unprecedented high channel number for high resolution imaging radar. Those innovations attract new comers in automotive radar field for instance with Magna and also well established players through the whole supply chain: Infineon Technologies, Denso, Toyota, Hyundai… It will certainly reshape the competition with the current leaders Continental and Bosch.

Regarding automotive 77 GHz radar chips, today it is mainly based on a 130nm SiGe platform, with NXP and Infineon Technologies as the top suppliers. RFCMOS technology is entering the market with semiconductor companies such as Texas Instruments with an intermediate technology node of 45nm. And technology scaling has started with Analog Devices offering products based on advanced 28nm CMOS nodes and also foundries that are positioning their advanced process capabilities in this ecosystem. For example, Globalfoundries and its 22FDX platform support innovative start up Arbe Robotics with a 4D high resolution radar for autonomous cars.

“It is exciting to see such a wide diversity of technology offerings, a clear confirmation of the automotive radar market’s traction,” comments Cédric Malaquin from Yole. “However, penetrating the automotive market with new technologies is no easy task. On the contrary, entering and maintaining a position in the automotive supply chain is a long, trust-based process.”

“We are certainly entering a new “radar age”, with many developments, disruptive technologies, and new entrants positioning this technology as the primary sensor – along with imaging (cameras) for ADAS and autonomous vehicles”, comments Claire Troadec, Division Director, Power & Wireless Division at Yole.

{kind=link}