Solar Panels for Vehicles Market:

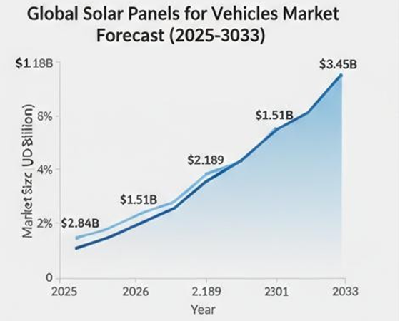

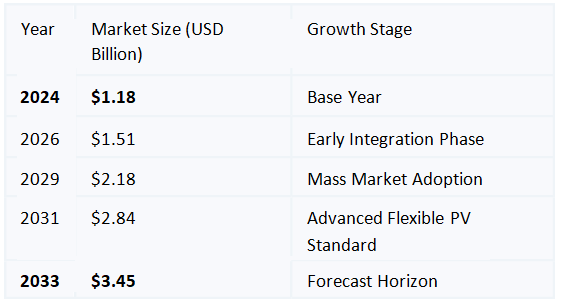

The Global Solar Panels for Vehicles Market is experiencing a transformative surge, projected to grow from USD 1.18 billion in2024 to USD 3.45 billion by 2033, at a robust compound annual growth rate (CAGR) of 12.6%. This expansion is propelled by an intensifying global focus on reducing greenhouse gas emissions, the rapid evolution of photovoltaic (PV) technologies, and rising demand for energy- efficient, range-extending solutions in the electric vehicle (EV) sector.

Integration of solar panels has moved beyond niche experimentation to become a strategic differentiator for automakers. As governments enforce stricter emission norms and incentivize clean technology, the adoption of vehicle-integrated solar panels is accelerating across passenger, commercial, and recreational vehicle segments.

The following trend reflects steady acceleration in market value as flexible, high-efficiency solar modules become standard in new vehicle designs.

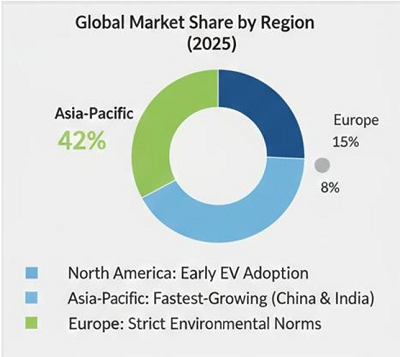

While North America currently maintains a leading position, the Asia-Pacific region is emerging as the primary engine for high-volume growth.

- North America (Largest Market Share): Dominated the market with an estimated share between 35% and 45% in 2025, fueled by early EV adoption and strong investments in renewable infrastructure.

- Asia-Pacific (Fastest Growing Region): Poised for rapid expansion with an expected 42% share in 2025, driven by China’s massive EV production scale and India’s initiatives promoting renewable integration.

- Europe (Significant Growth): Driven by stringent environmental laws and aggressive targets for decarbonizing the transportation sector.

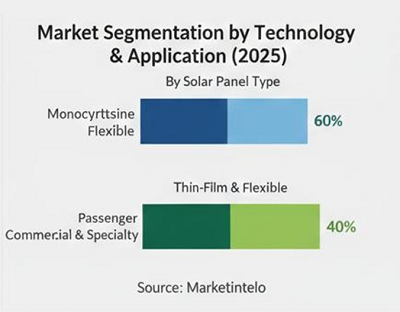

The market is increasingly defined by the efficiency of solar cells and their specific role within the vehicle’s power ecosystem.

- By Solar Panel Type:

- Monocrystalline (Dominant Segment): Accounted for approximately 45% to 63.9% of the market share due to its high energy conversion efficiency, crucial for limited vehicle surface areas.

- Thin-Film & Flexible Panels: Gaining traction for their ability to conform to curved vehicle bodies without adding significant weight or compromising aerodynamics.

- By Application:

- Passenger Vehicles: Currently the largest segment, holding roughly 58% to 65% of the market, driven by consumer demand for eco-friendly personal transportation.

- Commercial & Specialty Vehicles: Growing rapidly in logistics and public transport, where solar-assisted buses and delivery vans help lower operational costs.

Technological Pillars and Trends

The market’s foundation is shifting from rigid panels to sophisticated, integrated systems:

- Vehicle-Integrated Photovoltaics (VIPV): Panels are now integrated directly into body structures such as rooftops, hoods, and doors to reduce dependency on grid charging.

- Range Extension: Solar panels can add significant daily range; for instance, some integrated roofs add roughly 6 km to 70 km of driving distance per day under optimal conditions.

- Battery Charging Dominance: Applications dedicated to battery charging are expected to hold a 40% share by 2025, directly extending the range of electric and hybrid models.

Competitive Landscape

Key industry leaders and innovative companies pushing the boundaries of solar mobility include:

- Tesla Inc. & Toyota Motor Corporation

- Hyundai Motor Company & Ford Motor Company

- Nissan Motor Corporation & Volkswagen

- Sono Motors & Lightyear

- Aptera Motors & BYD Auto Co. Ltd.

Conclusion

The solar panels for vehicles market stands at a critical juncture where environmental necessity meets technological maturity. While high initial manufacturing costs and durability challenges persist, the transition toward a USD 3.45 billion market by 2033 reflects a global commitment to energy-autonomous, green mobility.

For more information, visit Solar Panels for Vehicles Market

{kind=link}