Automotive electronics is the largest application scenario for MCUs. IC Insights expects global MCU sales to grow 10% to a record high of $21.5 billion in 2022, with automotive MCUs outpacing most other end markets. More than 40% of MCU sales come from automotive electronics, and automotive MCU sales are expected to grow at a CAGR of 7.7% over the next five years, outpacing general-purpose MCUs (7.3%).

At present, automotive MCUs which belongs to Embedded IC are mainly 8-bit, 16-bit and 32-bit, and different bits of MCUs play different jobs. The main distinction between a microprocessor and a microcontroller is that the former simply has a central processing unit, while the latter has a CPU, memory, and I/O all built into a single chip. Specifically: 8-bit MCU is mainly used for more basic control functions, such as seats, air conditioning, fans, windows, door control modules and other controls. 16-bit MCU is mainly used for the lower body, such as the engine, electronic brakes, suspension systems and other power and transmission systems. 32-bit MCUs fit into automotive intelligence and are mainly used for high-end intelligence and safety application scenarios such as cockpit entertainment, ADAS, and body control.

At this stage, the performance and memory capacity of 8-bit MCUs are growing, together with their own cost-effectiveness, they can replace some of the 16-bit MCU applications and are also backward compatible with 4-bit MCU applications. The 32-bit MCU will play an increasingly important role in the entire automotive E/E architecture of the master, can manage the four scattered low-end ECU units, the use of the number will continue to increase.

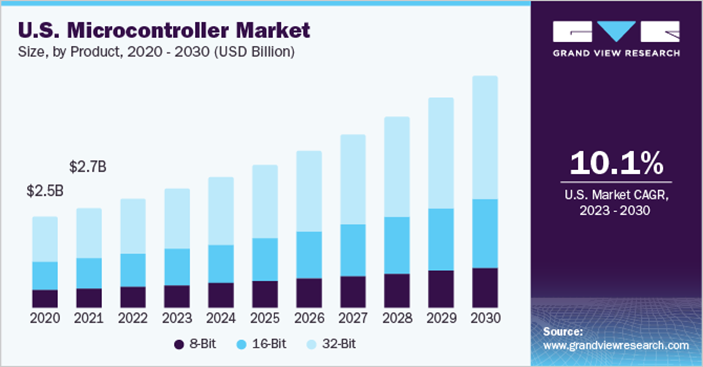

The above situation makes the 16-bit MCU is in a relatively embarrassing position, high not low, but in some application scenarios, it still has a place, such as some of the key applications of the powertrain. Automotive intelligence significantly boosted the demand for 32-bit MCUs, according to McClean report, in 2021, more than three-quarters of automotive MCU sales from 32-bit MCUs is expected to reach about 5.83 billion U.S. dollars; 16-bit MCU revenues of about 1.34 billion U.S. dollars; and 8-bit MCUs of about 441 million U.S. dollars.

And from the application level, infotainment is the application scenario with the highest year-on-year increase in automotive MCU sales, with a 59% increase in 2021 compared to 2020, and the rest of the scenarios had a 20% increase in revenue. Now all the electronic control of the car to use ECU (electronic control unit), and MCU is the core control chip of the ECU, each ECU has at least one MCU, so the current stage of intelligent electrification transformation and upgrading prompted the demand for MCU single-vehicle dosage of the demand for enhancement.

The strong demand for MCUs from automakers will be especially evident in 2021, when there will be a shortage of cores due to the epidemic. That year, many car companies because of the lack of core had to briefly shut down part of the production line, but automotive MCU sales soared 23% to $ 7.6 billion, a record high. Most of the automotive chips are produced on 8-inch wafers, and some vendors such as TI have shifted to 12-inch lines, and IDM will also outsource some of its production capacity to OEMs, which is dominated by MCUs, with about 70% of the production capacity borne by TSMC. However, the automotive business itself accounts for a very small proportion of TSMC, and TSMC heavy in the field of advanced process technology in consumer electronics, thus making the automotive MCU market seems particularly tight.

MCU competitive landscape as the entire semiconductor competitive environment, overseas giants dominate. 2021, the top five MCU vendors are NXP, Microchip, Renesas, STMicroelectronics, Infineon, these five MCU vendors accounted for 82.1% of the total global sales, compared with 72.2% in 2016, the head of the scale of the enterprise in the intervening years more and more growing. Automotive MCU market head effect is also significant, compared to consumer and industrial MCU, automotive MCU certification threshold is high, the certification cycle is long, the certification system includes ISO26262 standard certification, AEC-Q001 ~ 004 and IATF16949 standard certification, AEC-Q100 / Q104 Standard certification, of which ISO26262 for automotive functional safety is divided into four levels ASIL-A to D, such as the chassis and other scenarios of the highest security requirements, the need for ASIL-D level of certification, to meet the conditions of the chip makers are very few.

China’s MCU manufacturers are mainly concentrated in low-end areas, 32-bit MCU, although still monopolized by overseas giants, but some domestic companies have taken off. The 32-bit MCUs of Jifa Technology, BYD Semiconductor, National Core Technology, Core Ocean Technology, Core Wang Micro, Qipuwei, Saiten Micro and Lingou Chuangxin have all passed the AEC-Q100 certification. Guorong Securities statistics show that most of the domestic mass production companies are able to pass the AEC-Q100 certification, but mainly concentrated in Garde1/3. Domestic manufacturers able to pass the ISO26262 certification is very small, and most of them are concentrated in the ASIL-B level.

{kind=link}