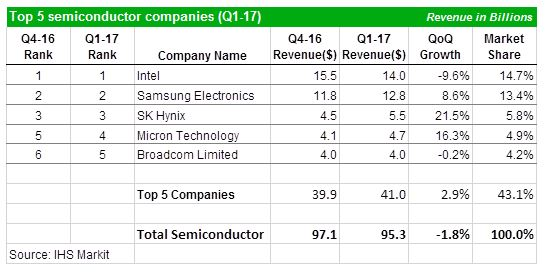

Following a strong fourth quarter, the semiconductor industry experienced a better than historical decline of 1.8% in the first quarter (Q1) of 2017. Global revenue came in at $95.3 billion, down from $97.1 billion in the prior quarter. This was a significant improvement over Q1, 2016 when the semiconductor industry declined by 8.6%.

Key Growth Drivers

According to Walter Coon, director at IHS Markit, the memory markets continue to be a driving force of semiconductor revenue expansion, with record revenues for both DRAM and NAND in Q1, 2017. NAND supply/demand dynamics remain extremely tight, with a healthy demand from SSD and mobile applications exceeding constrained bit supply due to the industry transition from planar to 3D NAND technology. With supply constraints persisting across both DRAM and NAND as we move into the second quarter, the memory market is poised to set even more records going forward.

The automotive sector proved to be a key growth driver in the semiconductor industry once again, posting a 4.7% growth over last quarter. Growth in this sector is being driven by increasing chip content in cars and the push towards electric vehicles (EVs). Content expansion and share gains are being enjoyed by all top players as demand remains high. Maxim Integrated was the first to mention a possible slowdown towards the end of the second quarter, due to weakness in the Chinese and US EV markets. Texas Instruments and Cypress disagreed, however, expressing more optimistic outlooks for the coming quarter.

NXP remains the top semiconductor supplier in automotive applications, even after its recent divestiture of its Standard Products division, which included discrete, logic and power MOS devices for many automotive applications. This division now operates as a stand-alone company, called Nexperia, following its acquisition by Chinese financial investors Wise Road Capital and Beijing Jianguang Asset Management in February. Infineon ranks number two, attributing its double digit growth rate in this sector to the strength in China and Europe in terms of their EV and ADAS businesses.

Among the top 20 semiconductor suppliers, while Intel remains in the number one spot for semiconductor suppliers, Analog Devices and SK Hynix enjoyed the highest revenue growth quarter over quarter by 29% and 21.5% respectively. Analog Devices achieved growth through its purchase of Linear Technology, making it an even bigger analog industry powerhouse. SK Hynix was driven by average sales price increases in both NAND and DRAM markets, as supply in the memory market remains tight.

More information on this topic can be found in the latest release of the Competitive Landscaping Tool from the Semiconductors & Components Service by IHS Markit.

More information on this topic can be found in the latest release of the Competitive Landscaping Tool from the Semiconductors & Components Service by IHS Markit.

{kind=link}