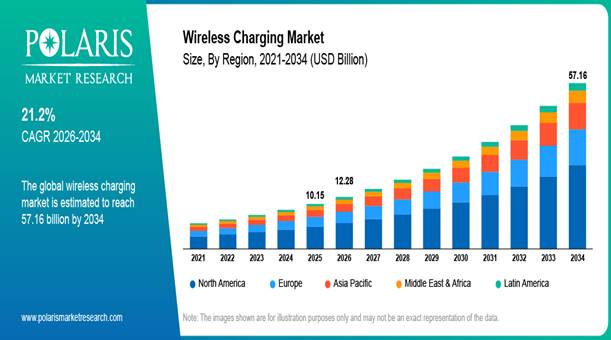

Wireless Charging Market – The global wireless charging market is on the cusp of explosive growth as cable-free power delivery moves from a premium smartphone feature to a mainstream expectation across consumer electronics, automotive, healthcare, and industrial applications. According to Polaris Market Research, the market was valued at USD 10.15 billion in 2025 and is forecast to climb to USD 12.28 billion in 2026, ultimately reaching USD 57.16 billion by 2034—a robust CAGR of 21.2% during the 2026–2034 forecast period. For a granular breakdown of technology segments, application forecasts, and competitive benchmarking, the full Wireless Charging Market Report is available from Polaris Market Research.

From Novelty to Necessity: The Cable-Free Shift

Once considered a convenience add-on, wireless charging—also known as inductive charging—has evolved into a core design expectation for modern electronics. By eliminating physical connectors, the technology enables sleeker device architectures, reduces port wear, and simplifies the user experience across smartphones, wearables, and increasingly, electric vehicles. As devices trend smaller and more water-resistant, wireless power transfer is emerging as an enabling technology rather than a peripheral feature.

Consumer Electronics: The Volume Driver

Consumer electronics remains the largest and fastest-accelerating application segment, projected to expand at a 22.3% CAGR through 2034, driven by surging demand for cable-free charging in smartphones, tablets, and wearables. Apple’s September 2024 launch of the iPhone 16 Pro Max Titanium—featuring a 4,865mAh battery supporting 15W wireless charging—illustrates how flagship devices continue to normalize wireless power as a standard capability rather than an accessory.

The inductive charging segment led the technology landscape with a 55.4% revenue share in 2025, owing to its cost-effectiveness, simplicity, and deep integration with the widely adopted Qi standard. The Wireless Power Consortium’s rollout of the Qi2 specification in 2023 has further accelerated compatibility and efficiency gains, addressing longstanding consumer concerns around charging speed and cross-brand interoperability.

Electric Vehicles Open a New Growth Frontier

Beyond consumer devices, wireless charging is gaining serious traction in electric mobility. Automakers and infrastructure providers are piloting in-ground and parking-based wireless EV charging systems that eliminate the need for physical connectors—a critical step toward autonomous and fleet-based mobility models. InductEV’s collaboration with Volvo Cars, showcased through a three-year deployment of 20 electric XC40 taxis in Gothenburg under Volvo’s Green City Zone initiative, achieved 100% uptime and demonstrated the commercial viability of wireless charging for autonomous taxi fleets.

Separately, WiTricity’s pilot with International Transportation Service at the Port of Long Beach is testing wireless charging performance on Ford E-Transit fleet vehicles in real-world logistics environments, while Valeo’s Ineez Air Charging system—operating at approximately 3kHz with Vehicle-to-Grid (V2G) capability—signals growing manufacturer investment in scalable, grid-compatible wireless EV infrastructure.

For more information, visit @ https://www.polarismarketresearch.com/industry-analysis/wireless-charging-market

Regional Dynamics: Asia Pacific Leads, North America Accelerates Fastest

Asia Pacific commanded the largest regional share in 2025, at 41.35% of global revenue, underpinned by a massive consumer electronics manufacturing base in China, Japan, and South Korea, along with rising EV adoption supported by regional government incentives.

North America, however, is projected to register the highest regional growth rate at 22.1%, driven by high penetration of premium consumer devices, strong R&D investment from technology leaders, and aggressive EV infrastructure buildout. California’s Clean Transportation Program—backed by up to USD 100 million in annual investment from the California Energy Commission—supports the state’s goal of 1.5 million zero-emission vehicles by 2025 and 100% ZEV sales by 2035, reinforcing the policy tailwinds behind wireless charging infrastructure expansion.

Component and Technology Outlook

By component, receivers held a 34.7% share in 2025, reflecting their deep integration into consumer electronics. Emerging technology variants are also broadening the addressable market: resonant charging supports multi-device and greater-distance charging suited to shared spaces, while radio frequency (RF) charging is gaining relevance for low-power IoT sensors and continuous-charge industrial applications.

Innovation Pipeline Signals Long-Term Momentum

Recent industry developments underscore the pace of innovation. In April 2026, ROHM Semiconductor introduced an ultra-compact wireless power chipset—the ML7670 receiver and ML7671 transmitter—purpose-built for miniaturized wearables such as smart rings and bands using 13.56 MHz NFC-based charging. Around the same time, Powercast demonstrated wireless power technology as infrastructure for battery-free sensing and edge-based data collection, aligning wireless charging with the growing computational demands of AI-driven edge devices. Belkin’s July 2025 achievement of Qi2 25W certification further reflects accelerating momentum toward faster, standardized wireless charging across the accessory ecosystem.

Competitive Landscape

The market features a mix of global technology leaders and specialized wireless power innovators, including Apple Inc., Qualcomm Technologies, Samsung, Powermat Technologies, Murata Manufacturing, Texas Instruments, Renesas Electronics, MediaTek, WiTricity Corporation, Energizer Holdings, Mojo Mobility, Powercast Corporation, ConvenientPower, Leggett & Platt, and Pluggless Power. Qualcomm’s 2011 acquisition of HaloIPT, a wireless EV charging specialist, exemplifies how established semiconductor players are expanding into automotive-grade wireless power to capture emerging revenue streams beyond mobile devices.

Challenges and Restraints

Despite strong tailwinds, the market faces adoption barriers. Wireless charging systems generally cost more than wired alternatives, and compatibility remains largely confined to Qi-enabled devices. Charging speeds, while improving, still lag behind high-wattage wired fast-charging in many use cases—a gap the industry is actively working to close through resonant and multi-coil innovations.

Outlook: A Cable-Free Future Takes Shape

With rising investment in long-range and fast wireless charging technologies, expanding smart home and smart vehicle ecosystems, and growing standardization efforts, wireless charging is positioned to become foundational infrastructure across consumer, automotive, healthcare, and industrial environments over the next decade.

For comprehensive segmentation data, country-level forecasts, and detailed competitor profiling, explore the full report: Wireless Charging Market Size, Share & Growth Analysis, 2026–2034 — Polaris Market Research

Read More @ https://www.polarismarketresearch.com.

Validation Solution for AI Networks")

{kind=link}